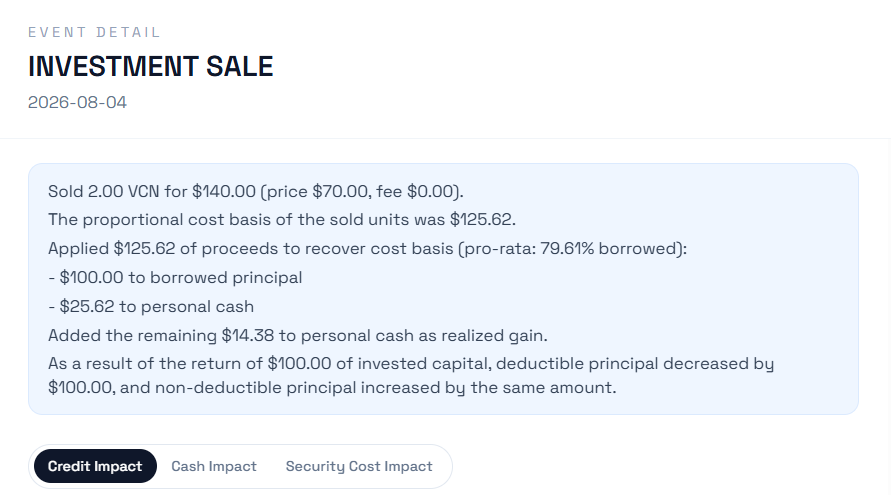

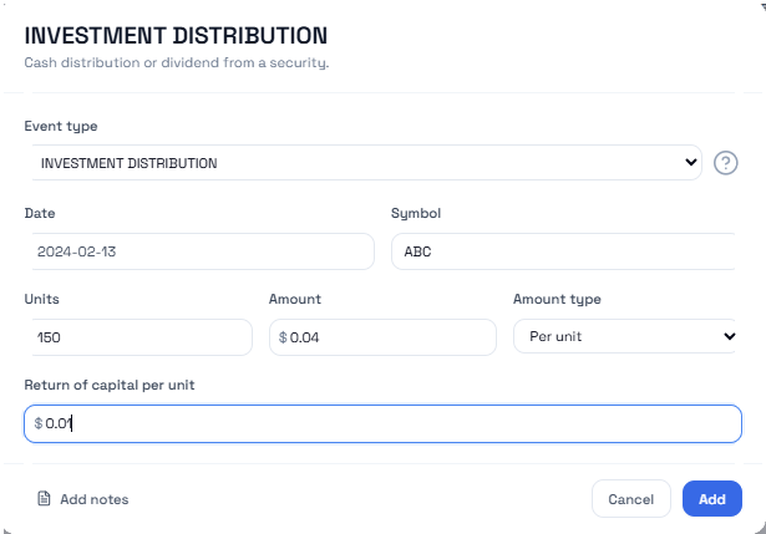

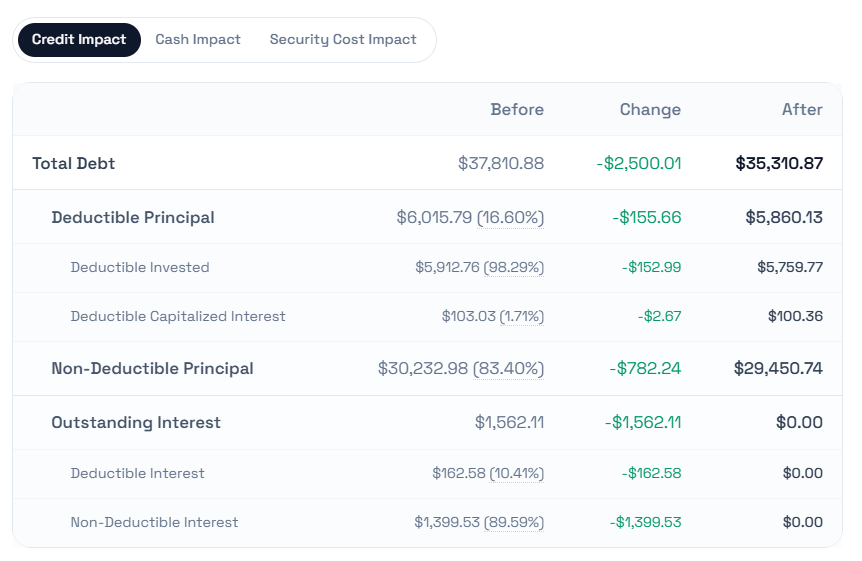

Plain-English explanations for every event

Open any event — a sale, distribution, payment, margin interest charge, or refinancing transfer — and see exactly what changed, why it changed, and how the deductible split moved. No formulas to reverse-engineer.

How events work →